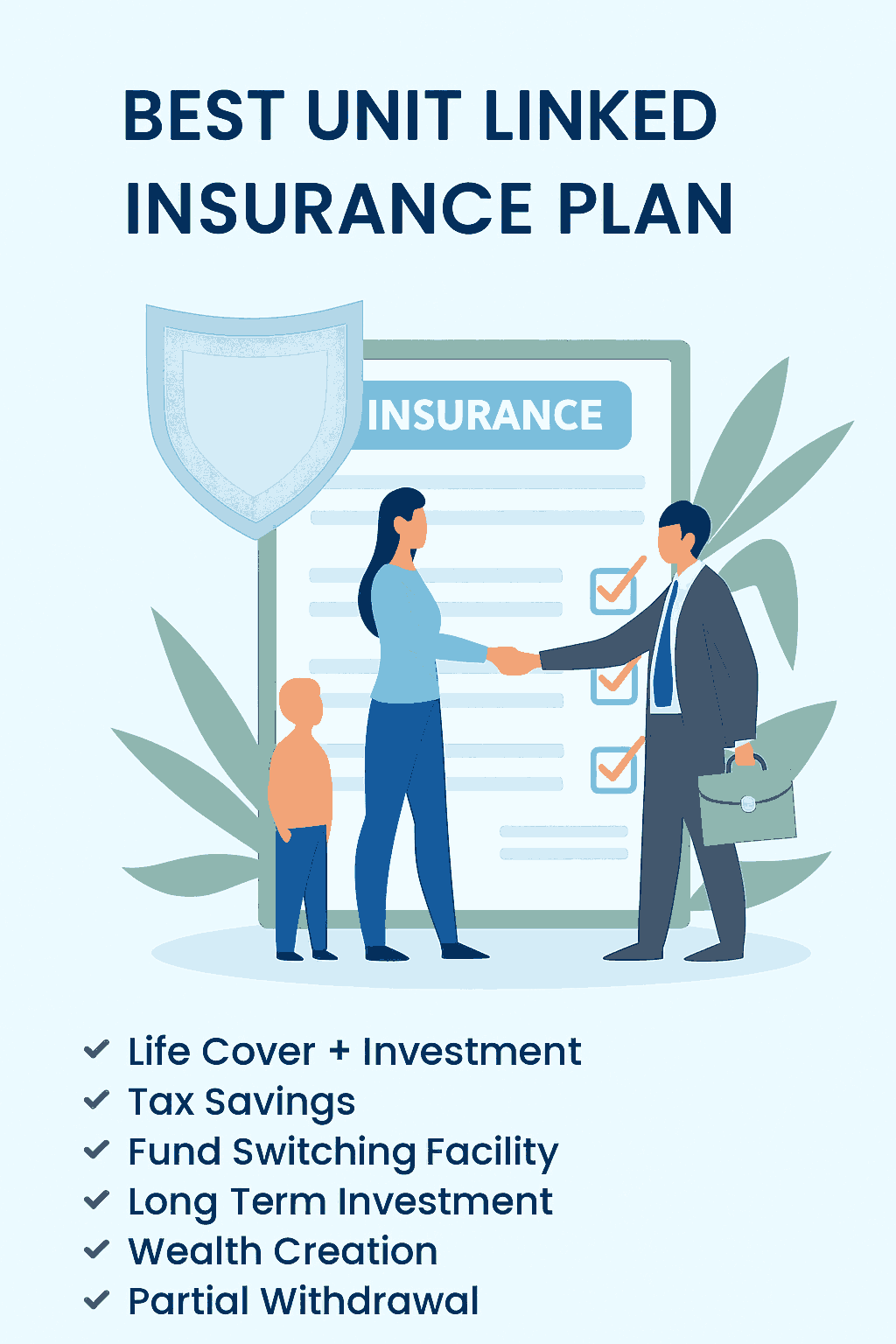

When it comes to a matter of balancing insurance and investment, the Unit Linked Insurance Plan (ULIP) is one of the most preferred options. Today many investors are looking for the best ULIP project with high income to ensure wealth creation, retirement plan and the future of their children. In this guide, we will explore different aspects of Ulip, compare projects and help you find a better ULIP project for your financial goals.

Unit Linked Insurance Plan (ULIP) is a unique financial product that combines life insurance and investment benefits. If a part of your premium provides life protection to your family, the other is invested in market-related funds (equity, loan or hybrid), which gives you the opportunity for growth.

Dual Benefits – Protection + investment under a single policy.

Long-Term Wealth Creation – Market-linked returns over 10–20 years.

Flexibility – Choose funds (equity, debt, hybrid) as per risk appetite.

Tax Advantages – Benefits under Section 80C and 10(10D).

Goal-Oriented Planning – Ideal for retirement, child education, or wealth creation.

ULIP with highest NAV performance offers maximum growth potential.

Switching option between funds to balance risk.

Lock-in period of 5 years ensures disciplined investing.

Partial withdrawal facility for emergencies.

Transparency in fund allocation and charges.

| Financial Goal | Recommended ULIP Type | Why It’s Best |

|---|---|---|

| Long-Term Growth | ULIP with highest NAV performance | Ensures higher wealth accumulation. |

| Retirement | Best ULIP for retirement planning | Provides stability and long-term income security. |

| Child’s Future | Child education ULIP plans | Ensures your child’s education expenses are covered even in your absence. |

| Wealth Creation | Wealth creation through ULIPs | Helps build a strong financial portfolio with market growth. |

Check Past NAV Performance

Look for ULIPs with a history of consistent growth and highest NAV performance.

Match with Your Financial Goals

For retirement: go with the best ULIP for retirement planning.

For child’s education: opt for child education ULIP plans.

Evaluate Fund Options

Ensure the ULIP scheme allows switching between equity and debt funds.

Understand Charges

Look for ULIPs with low allocation and administration charges to maximize returns.

Long-Term Commitment

The best ULIP scheme works best when you stay invested for 10+ years.

Insurance Coverage

Ensure the policy offers adequate life cover along with investments.

"I have invested in Ulip 12 years ago with the goal of my daughter's education. The combination of insurance and stable fund performance gave me peace of mind. Today, I can confidently say that this is the best decision for long -term security." - R. Sharma, Mumbai

Q1. What is the minimum lock-in period for ULIPs?

The minimum lock-in period is 5 years, then partial withdrawal is allowed.

Q2. Which is the best ULIP scheme for long-term growth?

Ulip is the best NAV performance and equity fund exposure to long -term growth.

Q3. Can ULIPs be used for retirement planning?

Yes, the best Ulip for the retirement plan provides a safety network for the collection of wealth and post -retirement.

Q4. Are ULIP returns guaranteed?

No, Ulip income is market-related. However, maintaining prolonged investment reduces risk and increases revenue.

Q5. Can I switch funds within my ULIP?

No, Ulip income is market-related. However, maintaining prolonged investment reduces risk and increases revenue.

Choosing a better ULIP project with high income is about setting up your financial goals with the right plan. Whether it is a retirement plan, whether children's education is Ulip or Ulip, Ulip, Ulip provides flexibility, development and protection in a single package. By committing to a long -term strategy and evaluating NAV performance, you can increase the benefits and achieve your financial dreams.

.jpg)

.jpg)

.png)

.png)

.png)